In this piece. Traditional credit data is a record of what a borrower did before they applied. Vision Score reads a biometric signal your onboarding already captures at the point of application, and turns it into an independent credit risk score that runs alongside your existing model. Here is what that signal is, why it is already sitting in your workflow unused, how it handles the customers you already have, and how it has performed in the field.

We recently looked at why Philippine loan defaults keep rising even as credit data reaches record coverage. The short version: every model in use was built to read the past, and the fastest-growing borrower segment is the one the past can barely describe. This piece is about the part of the answer that is already sitting inside your own onboarding flow.

The 11pm application

A loan application lands at 11pm. On paper, it checks out. Steady income, a clean record, every document in order. The model approves. Six months later the account is in collections, and nothing in the file saw it coming.

Every risk team has some version of this story, and its mirror image: the applicant who looked thin or unscoreable, got declined, and would have paid every installment on time. Both have the same problem wearing different clothes. The information you underwrite describes what the borrower did before they applied. It says very little about the application in front of you.

That gap is where Vision Score works.

What Vision Score actually reads

Your model reads their record. Vision Score reads their application.

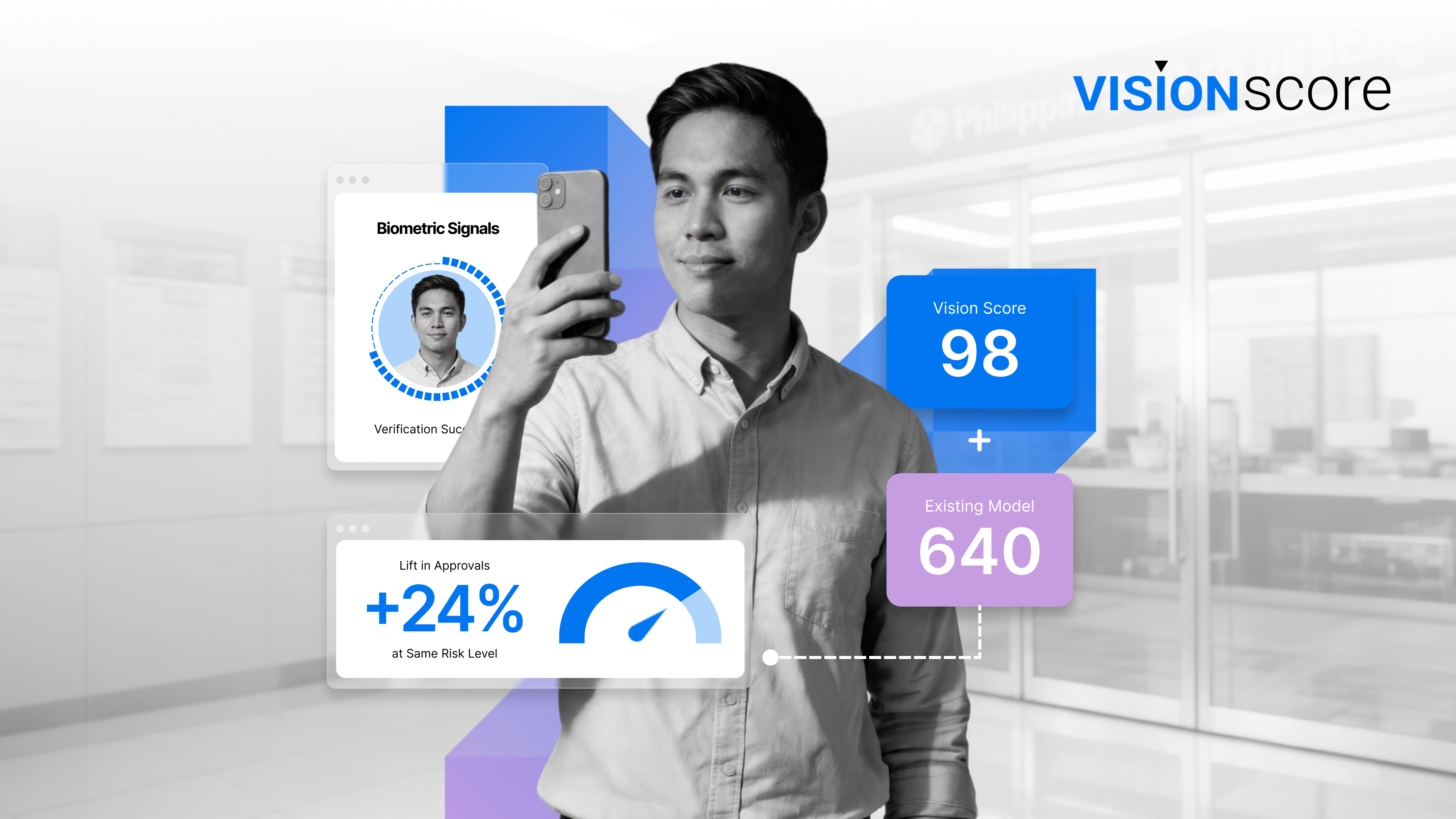

Traditional data tells you what a borrower did: what they borrowed, repaid, and owed. It is a record, reported and aggregated over time, and it is strong for borrowers who have one. Vision Score reads something different in kind. When an application comes in, computer vision models analyse a biometric signal captured during the borrower's own onboarding, and return a single independent score, 0 to 100. Not a report of past behaviour, but a signal drawn from the application itself, of a category no financial file contains.

You are already capturing this signal

Here is the part most lenders have not clocked. That signal is already in your workflow.

During digital onboarding, your system captures a biometric signal as part of standard identity verification. Liveness checks confirm a real, live person is applying. Age estimation and environmental cues from the capture help validate the applicant. All of it is used to confirm identity, and then set aside. The credit risk information carried in those same signals has never been extracted.

That is the whole idea behind Vision Score. It does not ask the borrower for anything new and it does not add a step. It reads the risk signal in a capture you are already collecting, and hands your model something it has never had. One API call, inside the flow you already run.

In live onboarding, that read happens in the present, at the moment of application. That is where the frame comes from: your model knows their past, Vision Score reads their present. But the signal lives in the image, so it is not confined to the moment of capture, which matters for the customers you already have.

How it fits your stack

The question we hear most is whether this replaces the model a lender already trusts. It does not, and that is a design choice, not a limitation.

Vision Score is an independent layer. It runs alongside your existing model through a single API, and your decisioning logic sets how much weight it carries. You keep full control of the decision. It connects to the origination, onboarding, or payment workflow you already have, and a full validated deployment typically runs in three to six weeks, not months.

Think of it as adding a sense, not swapping a brain. Your model still does what it does well. Vision Score gives it access to a signal it has never been able to read.

It also works on the book you already have

Because the signal lives in the image, Vision Score is not limited to new applications. You can run it on the onboarding images you already hold, including customers whose application was years ago.

Lenders use this two ways. First, to validate the signal on their own portfolio before deploying it on anyone new, scoring a book with known outcomes to see how it performs. Second, to re-assess an existing book, surfacing risk in accounts your model only ever scored on history. Same independent read, applied to borrowers you already have.

Built to sit inside your compliance structure

In a market this sensitive to biometric data, how a product is deployed matters as much as what it does. Vision Score is built to fit the compliance structure a regulated lender already runs, with accountability clearly divided.

You stay the data controller and own the customer relationship, the consent, and the decision, as you already do under BSP and Data Privacy Act obligations. We operate as your processor, under your instruction and accountable for how the model performs and how the data is handled. Vision Score never interacts with your borrowers directly. It supports the decision; it never makes it alone, and it does not classify people.

What it reads is deliberately narrow: non-sensitive properties of the capture, like image integrity, consistency, and resistance to spoofing. Protected attributes, including race, ethnicity, skin color, and nationality, are excluded from the model by design. Because that alone does not guarantee a fair outcome, fairness is tested against the EEOC Four-Fifths Rule across race, gender, age, and skin tone, and re-tested on every model update.

Privacy is handled the same way: data minimization, encryption, strict access controls, and defined retention and deletion, with on-premise deployment inside your own environment available where required. The full Responsible AI, Fairness, and Model Governance Statement is available on request.

By the numbers

The signal is only worth adding if it holds up to scrutiny, so here is what it rests on.

Vision Score is validated on more than a million real-world loan outcomes, and it delivers a minimum 30% Gini coefficient as a standalone signal, a credible, measurable read on risk even for first-time borrowers with no credit history. It returns an independent score from 0 to 100 inside your existing flow.

Fairness is tested the hard way. Vision Score was put through 30 independent adverse-impact checks across race, gender, age, and skin tone, and passed all 30, with zero violations. The signals it reads do not translate into disadvantage for any protected group. And in model-based projections, lenders adding it to their decisioning have seen credit losses reduced by up to 20%.*

What it looks like in the field

Vision Score has been validated with lenders across Vietnam, Indonesia, and the Philippines, from consumer finance companies and a commercial bank to digital and online lending platforms. Different markets, different products, and the same pattern each time: risk concentrates in the lowest-scoring applicants, so filtering out a small worst-scoring slice removes an outsized share of the defaults while leaving the rest of the book untouched.

| Market | Lender Type | The Result |

| Vietnam | Consumer finance | On raw, unfiltered application traffic, the lowest-scoring 20% of applicants held close to half of all defaults, isolating the worst risk at the very top of the funnel |

| Vietnam | Commercial bank | Risk ranked cleanly across every score band on the lender's own sample, with defaults rising steadily from the best-scoring bin to the worst |

| Indonesia | Digital lending | Separated good from bad even for borrowers with no credit history, with roughly a fifth of all defaults caught in the worst-scoring 10% |

| Philippines | Online lending | Delivered a standalone Gini in line with the 30% floor, and the worst-scoring 20% of applicants captured over a quarter of all defaults |

In the Philippine deployment, filtering the worst-scoring 20% of applicants while keeping roughly 80% of volume removed a disproportionate share of the portfolio's defaults. That is the shape of the whole value proposition: more approvals and lower losses moving in the same direction. Full figure-level results are available under NDA.

What Vision Score is, and what it isn't

Trust comes from being clear about the edges.

It is an independent credit risk score, built on computer vision, that runs alongside your existing model and reads a biometric signal from the application. It is validated on real loan performance and calibrated to your book.

It is not a replacement for your scoring model. It is not a fraud or identity-verification tool; the output is a credit risk score, not a pass or fail. It is not based on physical appearance, and it is not trained to link any physical characteristic to creditworthiness. And it is not something the borrower has to learn, click, or do anything different for.

The bottom line

Your model is good at what it was built for: reading the record. The borrowers it struggles with, the ones who default despite a clean file and the ones who would have repaid despite a thin one, share the same blind spot. Both are decided on a record, and a record can only tell you so much.

The signal that fills the gap is already moving through your onboarding. Vision Score is what reads it. More right approvals, fewer wrong ones, and a portfolio that finally includes borrowers your data could never see.

See how Vision Score fits your portfolio. Book a demo, or read more on the Vision Score product page.